Last week, more than 300 professionals from across the industrial and logistics (I&L) sector came together to discuss the hottest topics and industry trends at Property Week’s Industrial & Logistics Conference, held at The Kia Oval in London.

The new normal: an expert panel addressed the new occupiers taking space

The sector has experienced a rollercoaster ride in the past few years. During the Covid pandemic, rents and net asset values rose rapidly, driven largely by increased ecommerce demand, before taking a turn for the worse in 2022, amid a broader economic slowdown.

However, last year, there were strong signs the sector was on the way back up. Data from agency Savills shows that take-up reached the highest level since 2022 by the end of the year.

In the opening panel session, ’Rethinking I&L for a new era’, delegates were told significant challenges remained despite the recent upturn.

Jonathan Wallis, managing director of Tritax Big Box Developments, said the planning system remained problematic for I&L developers. “There have been some good attempts in terms of grey-belt and green-belt land release and the positive assumption for development,” he said.

The sector could help the government achieve its growth objectives

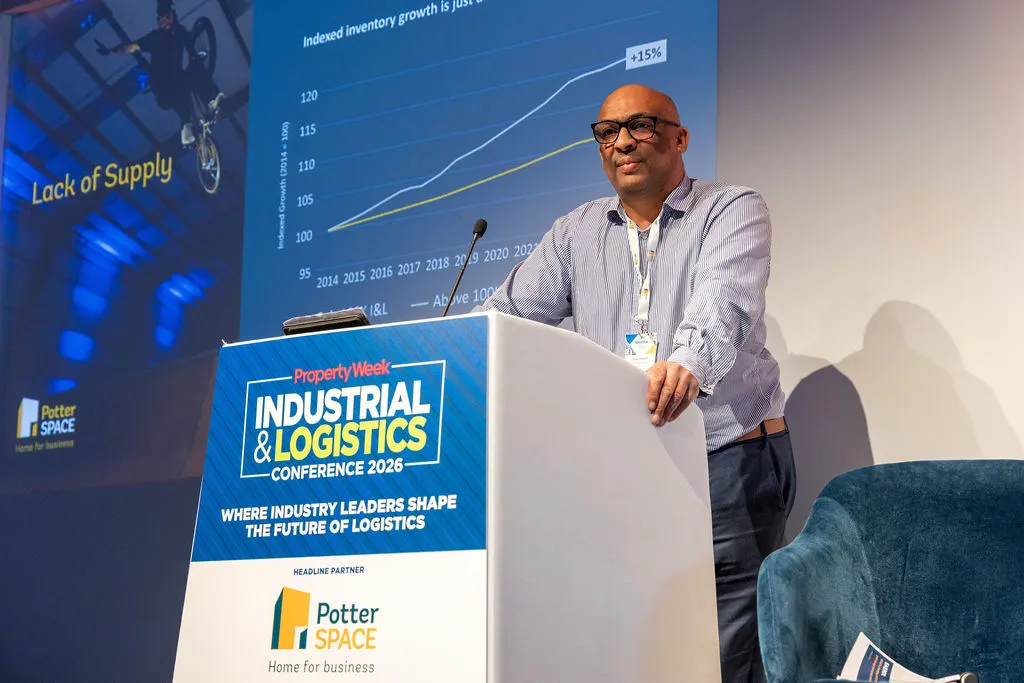

Jason Rockett, Potter Space

However, he also warned that local authorities “are in a worse state than they have ever been in terms of staffing, talent and finances, which has led to an absolute mess”.

Wallis pointed out that only 18% of planning applications were determined within the statutory 13-week period, while more than 60% were taking longer than a year to get determined. “On a national scale, there is good progress, but it’s not filtering down to the local level,” he concluded.

Dan Holford, SEGRO’s head of national markets, said the government must recognise that the I&L sector “is part of the backbone of the UK, whether it is data centres, ecommerce or manufacturing”.

He added that limited access to grid power was holding back I&L developments. “Data centre power demands are 10 times what they were in the 2000s,” he said. “The scale of the demand is greater than ever. Traditional I&L occupiers are also seeing their power needs expand exponentially. So, power is a growing concern.”

He added that limited access to grid power was holding back I&L developments. “Data centre power demands are 10 times what they were in the 2000s,” he said. “The scale of the demand is greater than ever. Traditional I&L occupiers are also seeing their power needs expand exponentially. So, power is a growing concern.”

A need for investment zones

Adrienne Howells, land director at SmartParc, which creates specialist food manufacturing and distribution centres, called for an extension of investment zones to include the food and beverage industry.

“The Netherlands is the second-largest food and beverage exporter, second only to the US, which is incredible considering their size,” she said. “They achieved that through exactly those types of investment zones specifically for that sector.”

During the panel session ‘Market realignment and the new normal for I&L’, Claire Williams, head of UK and European industrial research at Knight Frank, said there had been a dramatic growth in the take-up of UK I&L space from Chinese e-tailers.

She said retailer JD.com had taken over 1m sq ft since the start of last year, adding: “They’re planning to rival Amazon. They’re the largest but by no means the only Chinese ecommerce company in this space. Shein and Temu have also taken space.”

Williams said that these occupiers were also changing the shape of the market, as their expectations for lease flexibility and service levels were often different to standard UK practices.

However, Andrew Blennerhassett, associate director at Savills, cast doubt on whether Chinese e-tailers were growing the market overall. “Ecommerce growth is largely flat,” he said. “I question whether it’s more a case of multiple players taking a slice out of the same pie. But in the grand scheme of things, ecommerce remains a good driver of logistics.”

However, Andrew Blennerhassett, associate director at Savills, cast doubt on whether Chinese e-tailers were growing the market overall. “Ecommerce growth is largely flat,” he said. “I question whether it’s more a case of multiple players taking a slice out of the same pie. But in the grand scheme of things, ecommerce remains a good driver of logistics.”

At a presentation later in the day, Jason Rockett, managing director of conference headline partner Potter Space, underlined the importance of the smaller end of the I&L market. He said 95% of I&L units were below 100,000 sq ft, while small- to mid-box occupiers paid 62% of all I&L business rates, according to research Potter Space conducted with Savills. “The contribution to the economy is huge, but often overlooked,” he said.

Rockett added that the UK government’s industrial strategy, unveiled last June, was encouraging but he believed it needed to go further. “The sector could really help the government achieve its growth objectives – it cannot be ignored,” he said.

Land, power and planning

Meanwhile, in the debate ‘Data centres and the future I&L landscape’, Sophie Phillips, senior associate at law firm Bird & Bird, said the key challenges facing data centre development were “land, power and planning”.

She cited International Energy Agency research showing that global electricity demand from data centres will double to more than 945 terawatt-hours by 2030. “That is more than the entire electricity consumption of Japan today,” she noted.

Christian Goldsmith, data centre global solutions lead at Arcadis, said he did not believe that renewable energy could solve the power supply problem. “Data centres need certainty of supply,” he said. ”Any form of renewable energy dependent on weather conditions is not good for powering data centres.”

However, he did see opportunities to reuse heat generated by data centres within wider campus developments.

Debate at the conference made it clear that while the I&L sector faces challenges, the market’s fundamentals are strong and it is likely to remain one of the best-performing property asset classes.