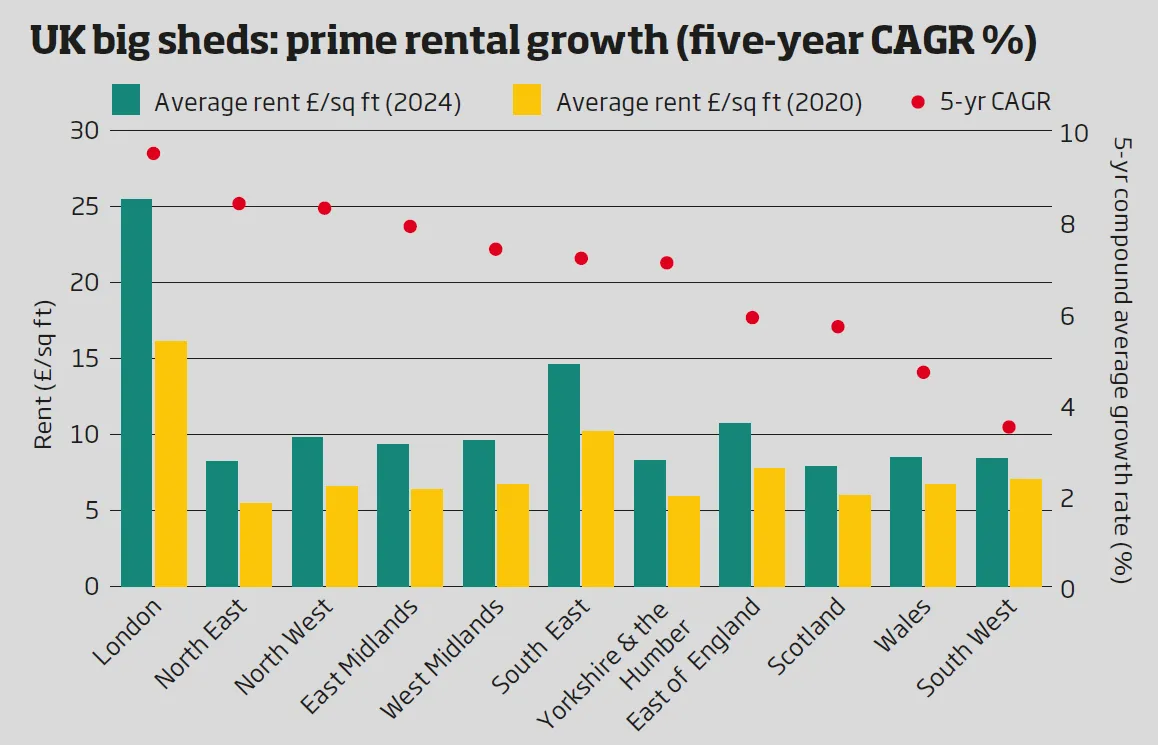

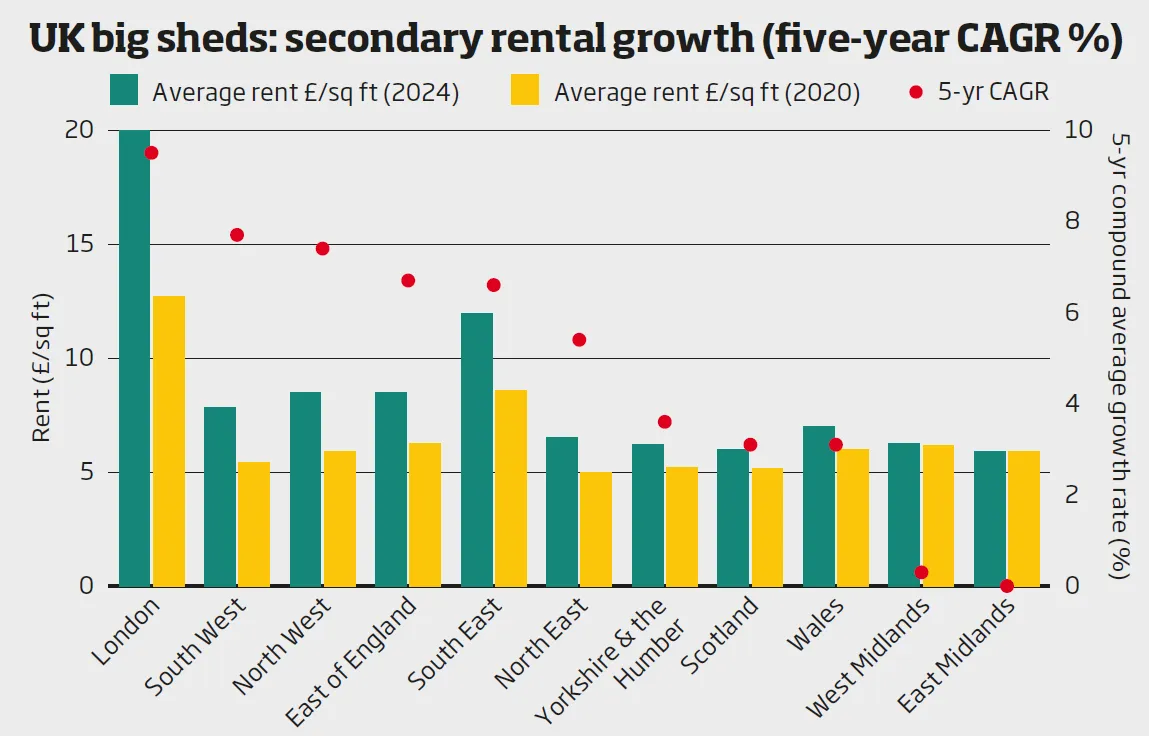

Rents for modern, 100,000 sq ft-plus warehouses have outpaced the rest of the big-sheds market, rising by a compound annual growth rate (CAGR) of 6.9% since 2020, compared with more modest 4.9% growth for secondary warehouses, Savills research shows.

Savills defines prime warehouses as speculatively built or modernised properties, while secondary stock consists of older warehouses that fail to meet high energy efficiency standards.

Savills defines prime warehouses as speculatively built or modernised properties, while secondary stock consists of older warehouses that fail to meet high energy efficiency standards.

At the end of 2024, rents for prime big sheds averaged around £11.00/sq ft and stood at £8.60/sq ft for secondary warehouses.

London remains the top-performing region across both the prime and secondary big-shed markets, achieving an average annualised growth rate of 9.5%.

Outside the capital, the North East and the North West were the top performers for prime rental growth, at 8.4% and 8.3% respectively, while the strongest regions for secondary rental growth were the South West (7.7%) and the North West (7.4%).

Logistics sites in the centre of the country continue to perform strongly, with the East Midlands and West Midlands recording prime rental growth of 7.9% and 7.4% respectively.

Logistics sites in the centre of the country continue to perform strongly, with the East Midlands and West Midlands recording prime rental growth of 7.9% and 7.4% respectively.

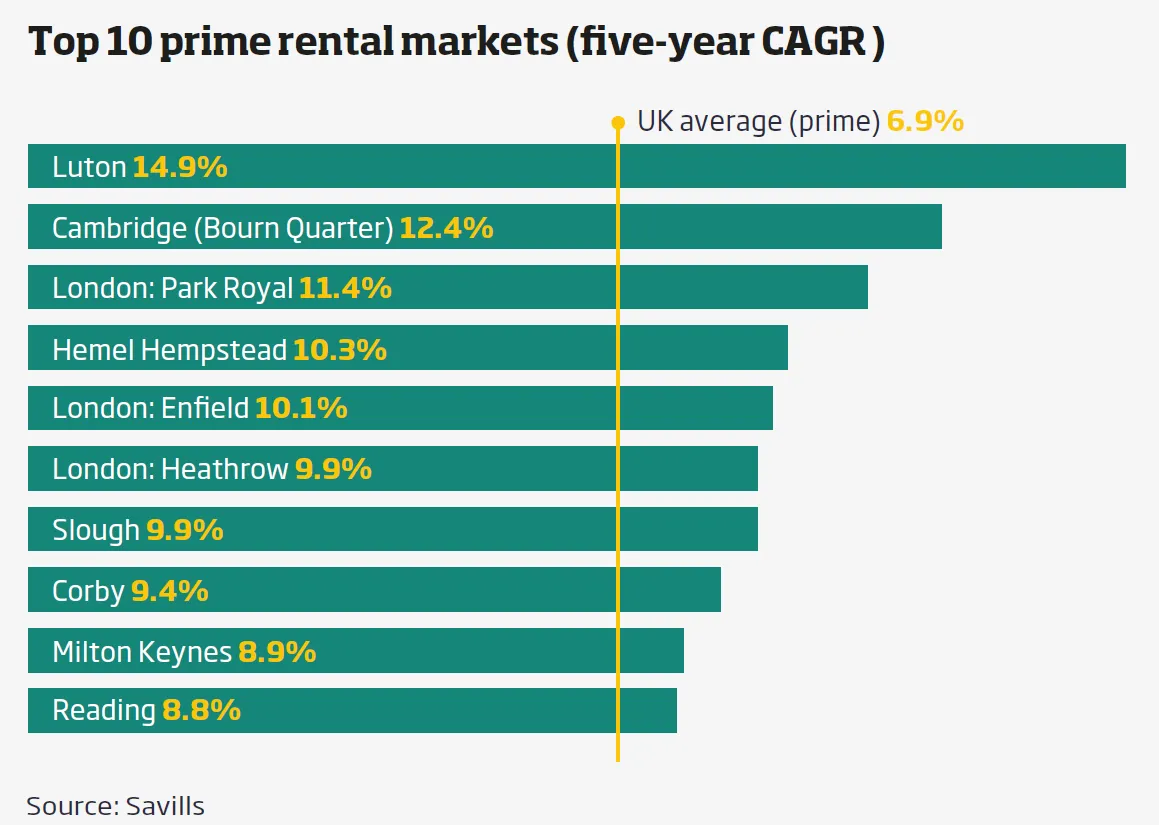

Lewis Rapley, associate in Savills’ industrial and logistics research team, says demand for warehousing in London remains particularly strong, driven by its strategic location, access to power and significantly constrained land supply.

“Consequently, growing demand for urban logistics provision, particularly in conurbations close to residential populations, has spurred further growth,” he adds. “This is evident in the numbers, with Park Royal and Enfield, for instance, achieving [average] annualised rental growth of 10.8% for prime rents between them and 11.1% for secondary rents.”

However, Savills expects current economic uncertainty and increased costs for employers to have an impact on demand for warehouse space.

Rapley says vacancy rates for large warehouses stand at 7.6%, up slightly from 7.4% at the end of 2024, but there are “pockets of undersupply” in the market.

Rapley says vacancy rates for large warehouses stand at 7.6%, up slightly from 7.4% at the end of 2024, but there are “pockets of undersupply” in the market.

“As a result, it is likely that prime rental growth will be concentrated in areas where the supply and demand dynamics remain out of sync; whereas secondary market units where comprehensive refurbishments have taken place to bring the units up to modern ESG standards are expected to outperform,” he adds.